The $10,000 Loss Per Coin: Why Bitcoin Miners Are Fleeing to AI

Analysis of hardware repurposing strategies as cryptocurrency mining economics deteriorate, forcing capital investment into AI compute markets.

The math is brutal and uncomplicated. It costs the average publicly listed Bitcoin miner approximately $79,995 to produce a single coin. Bitcoin is trading around $70,000. That leaves a roughly $10,000 loss on every single block mined, a reality that has persisted for most of 2026. While crypto Twitter argues about whether this is a “temporary dip” or “the new normal”, the people actually running the machines have already voted with their feet. They’re unplugging the ASICs, retrofitting the cooling systems, and chasing the only revenue stream that currently prints money: AI infrastructure.

This isn’t a strategic pivot. It’s a distress signal with better marketing.

When the Hashprice Breaks

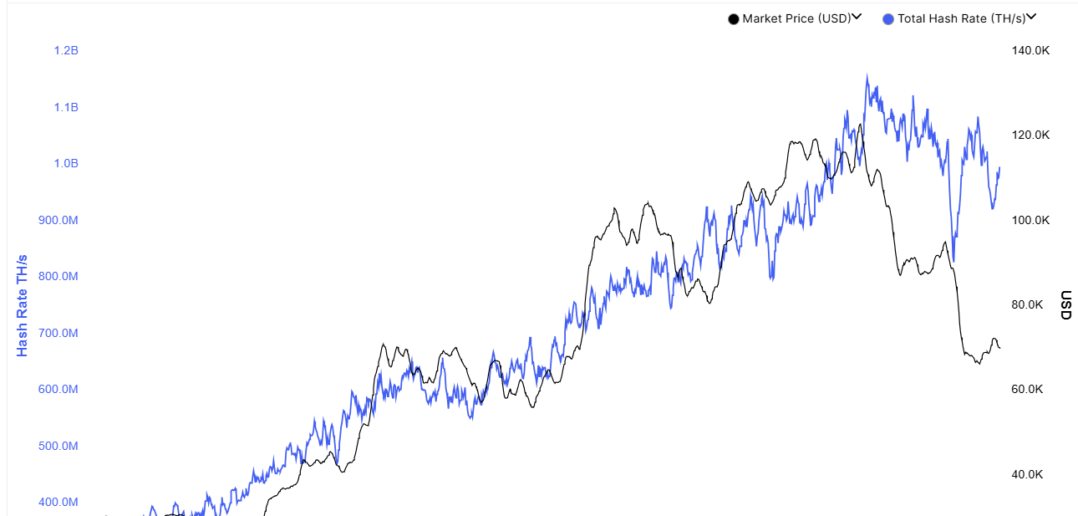

To understand why miners are dismantling their operations, you need to look at the hashprice, the daily revenue per petahash per second (PH/s) of computing power. This metric collapsed from $36-$38 per PH/s in late 2025 to roughly $28-$30 in early 2026, hitting an all-time post-halving low. The April 2024 halving had already cut block rewards from 6.25 BTC to 3.125 BTC, slicing revenue in half while electricity contracts and hardware debt remained stubbornly fixed.

The result? Between 15% and 20% of the global mining fleet is currently operating at negative margins. Operators running older hardware (S19-class machines and earlier) or paying above $0.05 per kilowatt-hour are underwater. The network hashrate, which peaked at approximately 1,160 exahashes per second (EH/s) in October 2025, has declined to roughly 920 EH/s, the first three consecutive negative difficulty adjustments since July 2022.

The difficulty adjustment mechanism, designed to maintain Bitcoin’s ten-minute block time, has become a guillotine for marginal operators. As unprofitable rigs shut down, the difficulty drops, which should help survivors, but only if they can survive long enough to see the adjustment.

The Infrastructure Arbitrage

Here’s where the story gets interesting from an architectural standpoint. Bitcoin mining facilities, high-density power, precision cooling, purpose-built compute centers with robust electrical infrastructure, map almost perfectly onto what AI data centers require. The astronomical costs of AI infrastructure have created a bizarre market dynamic where the stranded assets of crypto miners are suddenly valuable real estate.

Bitcoin Mining Costs

$700k – $1M per megawatt

Generating between $57 – $129 per megawatt-hour.

AI Infrastructure Costs

$8M – $15M per megawatt

Generating $200 – $500 per megawatt-hour.

But the revenue tells the real story. When you’re bleeding $10,000 per coin, those margins look like salvation.

Core Scientific & CoreWeave

An expanded agreement worth $10.2 billion over twelve years.

TeraWulf

Locked in $12.8 billion in contracted HPC revenue.

Hut 8

Signed a $7 billion, fifteen-year lease for AI infrastructure at its River Bend campus.

IREN (Iris Energy)

Secured $3.6 billion in GPU financing tied to a Microsoft contract.

These aren’t side hustles. These are existential bets that fundamentally redefine what these companies are.

Financing the Transition: Debt and Liquidation

The pivot requires capital that most miners don’t have. They’re acquiring it through two mechanisms, both of which carry profound implications for Bitcoin’s security model.

First: Debt Accumulation

- IREN: Carries $3.7 billion in convertible notes.

- TeraWulf: Holds $5.7 billion in aggregate debt.

- Cipher Digital: Issued $1.7 billion in senior secured notes, causing quarterly interest expenses to jump from $3.2 million to $33.4 million.

Second: Bitcoin Treasury Liquidation

Publicly listed miners have collectively sold more than 15,000 BTC from peak holdings. Core Scientific liquidated approximately 1,900 BTC worth $175 million in January 2026. Bitdeer reduced its treasury to zero in February. Even MARA quietly expanded its policy to authorize sales from its entire balance sheet reserve.

The miners selling Bitcoin to fund AI buildouts are the same entities whose operations secure the network. Every BTC sold to finance an HPC contract is a coin that was supposed to remain in treasury, supporting the long-term alignment between miner incentives and Bitcoin appreciation. That alignment is fracturing.

The Valuation Bifurcation

Wall Street has already priced this transition. Miners with secured AI and HPC contracts now trade at 12.3 times next-twelve-month sales. Pure-play Bitcoin miners trade at 5.9 times. The market is paying more than double for AI exposure, creating a perverse incentive where every miner watching their peers trade at 12x while they trade at 6x has a financial obligation to announce an AI deal, regardless of execution capability.

CoinShares estimates that roughly 30% of listed miner revenue already comes from AI and HPC activities, with projections reaching 70% by the end of 2026. This creates a strange new entity: the hybrid infrastructure firm that happens to mine Bitcoin on the side, rather than the other way around.

The geographic distribution is shifting too. The United States, China, and Russia still control roughly 68% of global hashrate, but emerging markets like Paraguay and Ethiopia are gaining ground, driven by HIVE’s 300-megawatt operation and Bitdeer’s 40-megawatt facility. These locations offer the cheap power necessary to survive the margin compression that is driving US-based operators toward AI.

The Security Budget Problem

Here’s the uncomfortable truth that most coverage misses: If significant hashrate migrates permanently from Bitcoin mining to AI infrastructure, Bitcoin’s security budget faces a structural crisis. The network’s security depends on miners having a financial incentive to keep running. If the better business is hosting Nvidia GPUs instead of SHA-256 mining rigs, that incentive weakens.

CoinShares projects global hashrate could reach 1.8 zetahashes by end of 2026, but that projection assumes Bitcoin recovers toward $100,000. If it stays at $70,000 or below, the firm expects additional miner capitulation and continued acceleration of the AI pivot. The hashrate recovery projection and the AI pivot are in direct tension, you cannot have both if prices stay depressed.

Next-generation hardware offers a potential lifeline. Bitmain’s S23 series and Bitdeer’s SEALMINER A3, both operating below 10 joules per terahash, could roughly halve energy costs compared to current mid-generation fleets. But deploying new mining hardware requires capital, and that capital is currently flowing toward AI contracts instead.

Architectural Implications of AI at Scale

The architectural implications of AI at scale extend beyond simple hardware repurposing. These facilities require fundamentally different networking, cooling, and power delivery systems. AI training clusters demand liquid cooling and high-bandwidth interconnects that Bitcoin ASICs never needed. The retrofit process isn’t just plugging in different machines, it’s a ground-up reconstruction of the data center stack.

Companies like Core Scientific and Hut 8 aren’t just changing their revenue models, they’re rebuilding their facilities to handle the thermal and electrical density of GPU clusters. This represents a massive capital expenditure gamble that assumes the AI boom continues long enough to service the multi-billion-dollar debt loads now sitting on these balance sheets.

The Only Variable That Matters

The entire question of whether this is a temporary response or a permanent structural shift comes down to Bitcoin’s price. At $100,000, mining margins recover, hashprice rises toward $37 per PH/s, and the AI pivot slows. Companies that built AI infrastructure as a bridge can redirect attention back to mining with better economics. At $70,000 or below, the pivot accelerates. More coins get sold. More data centers get converted. More companies quietly stop calling themselves Bitcoin miners even if they keep a few rigs running for show.

The Bitcoin mining industry entered this cycle securing the network and accumulating coins. It is exiting as a group of companies that build AI data centers and sell Bitcoin to fund them. Whether that is a rational response to a temporary price dislocation or the beginning of something more permanent is the open question. The difficulty adjustment runs on schedule regardless. The blocks keep coming. But the companies keeping them coming are changing what they are, and the transition is moving faster than the market has priced in.

Summary:

- Infrastructure Opportunity: Purpose-built compute facilities with excess power capacity are available at distressed prices.

- Supply Pressure: Network security providers are incentivized to sell, not hold.

- The Bet: Miners are betting that the AI boom lasts longer than their Bitcoin treasury does.